Americans have a huge automotive debt problem right now. A new survey shows that 31 percent of American drivers who financed their car are underwater on their loans. The problem is even worse for EV owners – 46 percent of those folks have negative equity in their electric cars. Furthering the issue is the fact that over half of the drivers surveyed overestimated their vehicle’s value. Rough.

CarEdge – an automotive buying guidance website – carried out the survey in partnership with Black Book. They talked to about 1,000 drivers to figure out just how much financial trouble some folks were in when it came to their cars. The results are… not super great.

Here’s what the survey found when it comes to negative equity:

According to our survey, 31% of drivers who financed their vehicles are currently in negative equity. This number rises to 39% for vehicles purchased since 2022, indicating that newer car buyers are especially vulnerable. As vehicle prices increase and long loan terms become more common, the risk of being underwater is higher than ever.

[…]

Electric vehicle owners are significantly more likely to be underwater. Of the EV owners we surveyed, 46% are currently in negative equity, with a median loan-to-value (LTV) ratio of 0.94—higher than the broader market’s 0.73. Luxury car brands like Tesla and BMW also see higher rates of negative equity compared to budget brands like Toyota and Honda.

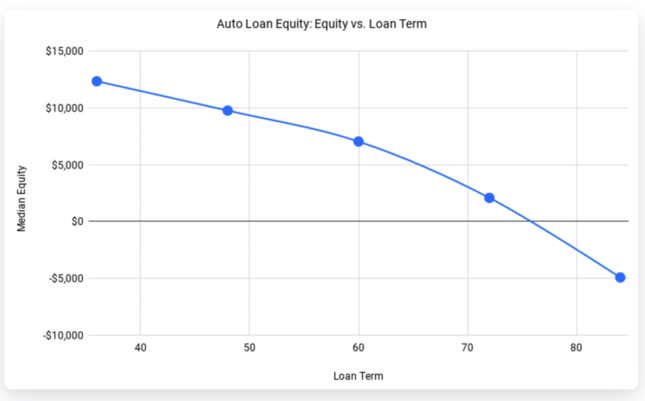

CarEdge says that loan terms directly impact a vehicle’s equity. Car owners with 84-month loan terms are about $5,000 underwater on average. On the flip side, buyers with a 36-month loan typically have about $12,340 in equity. Sure, longer loans reduce monthly payments, but they increase the likelihood of negative equity long term. That’s not something you should typically want out of a car purchase.

Something that really isn’t helping matters is the fact most people are greatly overestimating how much their cars are worth in the real world. CarEdge found that 61 percent of the folks surveyed think their car is worth more than it actually is. 17 percent say their car is worth at least $5,000 more than the true trade-in value. Not only is it something that’s a bummer to find out when it’s time to sell the car, but it can also lead to more buyers rolling over negative equity into their next car loan and continuing the cycle.

I’m really not sure what can be done. On one hand, folks are clearly going above their means to buy new cars. BUT, when the average price of a new car is over $48,000, it’s hard not to go above your means. Of course, there are cheaper options, and you can buy used, but damn. I feel like at some point this bubble is going to burst in a big way.